This multi-jurisdictional reference guide features a UAE chapter, authored by Shahram Safai (partner), Doneen Ennis (associate), Shruti Baghel (associate) and Anita Hajynia (paralegal) on the scope of corporate tax planning in the UAE.

Tag: Tax

Corporate Tax Return Filing: Key Considerations and Challenges

With the Corporate Tax regime now in force in the United Arab Emirates, there has been a significant shift in the country’s fiscal framework. Effective from June 1, 2023, the UAE Corporate Tax Law (Federal Decree Law 47 of 2022 on the Taxation of Corporations and Businesses) (CT Law) imposes corporate tax at the rate of 9% on taxable income exceeding AED 375,000 in a calendar year, while income up to this threshold remains taxable at the rate of 0%. With the first corporate tax return filing deadline approaching on September 30, 2025, it is essential for businesses to understand their return filing obligations, relevant deadlines, and potential challenges that may arise to ensure seamless compliance.

Under the CT Law, every taxable person, including juridical persons such as limited liability companies, public joint stock companies, free zone companies, and natural persons conducting business activities, is required to register for corporate tax and submit a corporate tax return with the Federal Tax Authority (FTA). Importantly, the requirement to file applies regardless of whether tax is payable or not by such an entity. Returns must be submitted electronically via the FTA’s online portal (EmaraTax), and only one corporate tax return is required to be filed, per tax period, as there are no provisions for advance or provisional returns.

Timeline: The timeline for filing a corporate tax return depends on an entity’s financial year. For businesses following a calendar year ending 31 December 2024, the first corporate tax return will be due on September 30, 2025. In general, the return must be filed within 9 months from the end of the relevant financial year of the entity, and any associated tax payment is due by the same deadline.

Penalties for non-compliance: In case of failure in timely filing of the return, a late filing penalty would be applicable, which is AED 500 per month, for the first 12 months and thereafter AED 1,000 per month. Further, late payment of tax would attract interest at the rate of 14% per annum on the outstanding amounts.

The UAE Corporate Tax regime offers several reliefs and incentives to reduce tax liability and support business growth. For example, eligible businesses with annual revenue up to AED 3 million can opt for Small Business Relief, effectively being treated as having zero taxable income for the relevant period. Additionally, Qualifying Free Zone Persons (QFZPs) enjoy a 0% tax rate on qualifying income, while group companies can benefit from tax-neutral transfers and business restructuring relief on mergers, demergers, or intra-group asset transfers.

Businesses may encounter several practical challenges when preparing and filing their returns. Some of the critical areas are discussed below:

Classification of income and expenses

Companies must distinguish between exempt income, such as dividends and capital gains on qualifying shareholdings, and taxable income, while also carefully identifying non-deductible expenses like fines, penalties, and certain entertainment costs. Misclassification in either category may result in overstated taxable income, underpaid taxes, or exposure to penalties.

Free Zone Regime

Although QFZP may benefit from corporate tax at the rate of 0% on qualifying income, derived from activities specified by the UAE Ministry of Finance, distinguishing between qualifying and non-qualifying income, particularly for service-based transactions across mainland or foreign jurisdictions can be complex. Even minor non-compliance with QFZP conditions may lead to loss of QFZP status for five tax periods, leading to unexpected tax liabilities.

Foreign Tax Credits

With respect to companies having presence in multiple jurisdictions, the CT Law allows for Foreign Tax Credits. Under such clause, taxes paid abroad can be credited against the UAE corporate tax liabilities, however, only the extent of the corporate tax payable on the same income. Even though it is a beneficial provision which may act as a relief to companies having presence in various jurisdictions, determining eligibility and quantum of credit, where foreign tax is not directly comparable to the UAE corporate tax, may be a challenge in direct availment of the benefit.

Corporate Tax Return Filing

To navigate these complexities effectively, businesses should take proactive steps to prepare well ahead of deadlines. Ensuring timely registration with the FTA, maintaining accurate accounting records, and aligning reporting systems with corporate tax requirements are critical for smooth compliance. Free zone entities should review their eligibility for preferential tax treatment and ensure the necessary substance and documentation are in place. Companies engaging in related-party transactions should evaluate their transfer pricing arrangements and prepare the required documentation early.

Thus, the corporate tax return is not just a compliance formality but requires careful application of the CT Law, Executive Regulations, and guidance issued by the FTA. Hence, it is of utmost importance that the companies engage tax advisors at an early stage in order to resolve issues which may become challenging at the time of finalisation of the tax return. Businesses that proactively manage their obligations will be better positioned to avoid penalties, optimise tax outcomes, and maintain a good standing with the authorities.

The Afridi & Angell tax team has been very active and busy advising clients on corporate tax law matters. Along with our affiliated tax agents and accountants, we can provide multi-disciplinary, knowledgeable and practical advice and assist in corporate tax strategy and tax return preparation. ■

The United Arab Emirates’ (UAE) Corporate Tax Regime: Globally Competitive and Business Friendly

Businesses often seek a favourable environment that fosters growth and offers tax savings. In this inBrief, we discuss the UAE’s tax-friendly landscape which stands out globally, drawing entrepreneurs, family offices and businesses that are eager to thrive in a jurisdiction with fewer restrictions and attractive exemptions and reliefs.

The UAE has become a major financial hub in the recent few years and is one of the easiest countries in which to do business. With the recent introduction of the Corporate Tax (CT) framework under Federal Decree Law 47 of 2022 (CT Law), the UAE aligned its fiscal policy with international tax standards and best practices, particularly pursuant to the goals of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS) project, which further solidifies the UAE’s position as a competitive business centre.

Tax Landscape

The UAE’s CT structure is designed to levy a modest 9% tax rate on businesses with profits (income after deduction of expenditure incurred wholly and exclusively for the purposes of a taxable person’s business) exceeding AED 375,000. This remains notably low compared to, for instance, Portugal, a traditionally favoured European country, with a 21% CT rate on profits exceeding €25,000 (approximately AED 95,000).

Portugal’s tax structure presents a notable contrast to the UAE’s, with implications for businesses. Portugal’s Value Added Tax (VAT) of 23% far exceeds the UAE’s 5%, in addition to levying a 25% withholding tax on dividends, interest, and royalties, adding complexity for businesses involved in cross-border trade. Comparatively, the UAE offers 0% withholding tax. Further, Portugal imposes a capital gains tax of up to 28%, while the UAE’s corporate tax rate is set at 9%.

Internationally Competitive and Connected

To facilitate and promote cross-border transactions and to continue to grow as a financial hub, the UAE has 137 Avoidance of Double Taxation Agreements and Bilateral Investment Treaties with other countries and the European Union (EU). These agreements are aimed at reducing double taxation and facilitating cross-border businesses. This approach encourages investment flows between treaty partners by reducing or even eliminating withholding taxes.

In addition, the UAE offers significant incentives to foreign investors through its 10-year Golden Visa program, which provides individuals with the opportunity to live, work, and invest in the UAE without the need for a local sponsor. The UAE also provides targeted incentives for technology and innovative startups, including funding opportunities, incubator programs, and tax exemptions to foster innovation and business growth.

No Personal Income Tax

One of the key advantages of the UAE’s favourable tax environment is the absence of personal income tax on wages, earnings, income from real estate investments and other types of investment income. This is in contrast to many European Union jurisdictions, where personal income tax rates often exceed 40% or even 50% for high-earning taxpayers.

Tax Relief and Exemptions

The CT Law provides for specific exemptions (for instance, the participation exemption), tax groupings for efficiency and preferential rates for qualifying small businesses and businesses engaged in specific sectors (innovation or technology). The aim of these tax exemptions and reliefs is to encourage corporate transactions, reduce the tax burden on emerging businesses and to stimulate economic growth within the UAE.

UAE Corporate Tax Law – A Business Attraction Tool

The UAE’s 9% CT rate, 5% VAT rate, absence of personal income tax (in most cases), 0% withholding tax rate, certain tax exemptions, international tax agreements and ease of doing business make it an unparalleled and highly competitive destination for multi-nationals, entrepreneurs, investors and family offices. As a result, the UAE CT regime acts as a tool to attract businesses to this highly business-friendly environment, especially in contrast to higher-tax jurisdictions in the EU, North America and Asia. ■

Capital Gains Tax Increase: Impact on Planning

The Canadian federal budget was tabled on 16 April 2024. It included, among other things, a proposal to increase the capital gains inclusion rate for the first time since 2001, from one half to two thirds, with the increase coming into effect for dispositions (or deemed dispositions) occurring on or after 25 June 2024 (and for individuals, the increase applies to capital gains over CAD 250,000 in any year, with capital gains below that amount remaining subject to the existing 50 percent inclusion rate).

Taxable capital gains (or losses) are realized when a Canadian resident sells a capital asset outside of a registered plan or qualifying insurance policy, and subject to some exemptions (e.g. lifetime capital gains exemption, principal residence exemption, reductions of inclusion rate on charitable donations). It is a common goal in Canadian tax planning to characterize as much personal and corporate income as possible as capital gains rather than other forms of income, because of the 50 percent inclusion rate (the other 50 percent being received tax free). Such planning will remain relevant as long as the capital gains inclusion rate is less than 100 percent; however, the increase to the inclusion rate will erode the benefit of doing so.

Examples of events or transactions which will be impacted by the increase include corporate surplus stripping transactions (which aim to extract corporate surplus as capital gains rather than dividends), estate freezes, taxes on death, and taxes on becoming non-resident of Canada. In addition, many professionals in Canada practice their profession through a professional corporation and accumulate and invest their savings in those corporations, virtually always pursuing a capital growth strategy because dividend income is taxed aggressively. The increase will impact the taxation of capital gains realized in those corporations.

Canadians may wish to consider deliberately triggering accrued capital gains prior to 25 June 2024 while the existing 50 percent inclusion rate is still applicable. This could entail crystalizing gains in investment accounts, carrying out an estate freeze, making lifetime gifts of capital property to family members or charities, or expediting plans to become non-resident of Canada (which triggers a deemed disposition of certain capital property upon exit).

Individuals with intentions to accumulate investment assets in private corporations and who would have otherwise planned to invest and grow their wealth in the corporation may now find that investing in corporate-owned life insurance is comparatively more attractive as well. Such policies and their in-policy growth continue to be tax-sheltered, and their comparatively conservative investment returns (versus unrestricted investment accounts) are less of a disadvantage in view of the higher capital gains inclusion rate.

Details of how the capital gains inclusion rate increase will be administered have not yet been released, particularly with respect to which transactions will be deemed to fall before and after 25 June 2024, and with respect to the inclusion rate for capital losses. It appears from the initial budget release that there will be an effort to match the inclusion rate for capital losses to capital gains at the same rate, likely to forestall triggering gains at the lower rate and losses at the higher rate on the same type of asset, such as public securities.

If you would like to pursue transactions to take advantage of the current 50 percent capital gains inclusion rate prior to 25 June 2024, or discuss becoming non-resident of Canada and related planning, please contact us and we will be glad to assist. ■

Developments in Corporate Tax Compliance

In the past week, guidance has been provided by both the Ministry of Finance and the Federal Tax Authority (FTA) regarding deadlines for Corporate Tax registration.

The new deadlines have the potential to significantly reduce the time left for meeting the deadlines for Corporate Tax registration. For example, certain applicable taxable persons will be required to submit the Corporate Tax registration applications by 31 May 2024 in order to avoid a violation and the applicable penalties.

Previous guidance from the FTA stated that taxable persons would have until the due date of their first tax return to register. For example, if a taxable person had a financial year ending on 31 May 2023, they would have a registration period of 26 months available until 28 February 2025. Similarly, for taxable persons with a financial year ending on 31 December 2022, a registration period of 33 months would be available until 30 September 2025.

Federal Tax Authority Decision No 3 of 2024 (FTA Decision) was issued on 22 February 2024 mandating specific application deadlines to register for Corporate Tax applicable to both juridical and natural persons, that are either resident or non-resident persons, to be effective from 1 March 2024.

We emphasise that the deadlines are applicable for the submission of Corporate Tax registration applications, as distinguished from completion of the registration process and possession of a registration certificate.

The deadlines specified by the FTA Decision are determined by a combination of the month of issuance of the taxable person’s Trade License, whether a juridical person was incorporated prior to 1 March 2024, and the residency of the taxable person.

Tax Registration Deadlines of Resident Juridical Persons

A juridical person that is a Resident Person, incorporated or otherwise established or recognised prior to 1 March 2024, shall submit the Tax Registration application, in accordance with the following:

Date of License Issuance Irrespective of Year of Issuance | Deadline for submitting a Tax Registration application |

1 January – 31 January | 31 May 2024 |

1 February – 28/29 February | 31 May 2024 |

1 March – 31 March | 30 June 2024 |

1 April – 30 April | 30 June 2024 |

1 May – 31 May | 31 July 2024 |

1 June – 30 June | 31 August 2024 |

1 July – 31 July | 30 September 2024 |

1 August – 31 August | 31 October 2024 |

1 September – 30 September | 31 October 2024 |

1 October – 31 October | 30 November 2024 |

1 December – 31 December | 31 December 2024 |

Where a person does not have a License at the effective date of the FTA Decision | (3) three months from the effective date of the FTA Decision |

A juridical person, that is a Resident Person incorporated or otherwise established or recognised on or after 1 March 2024, shall submit the Tax Registration application, in accordance with the following:

Category of Juridical Persons | Deadline for submitting a Tax Registration application |

A person that is incorporated or otherwise established or recognized under the applicable legislation in the UAE, including a Free Zone Person | (3) three months from the date of incorporation, establishment or recognition |

A person that is incorporated or otherwise established or recognized under the applicable legislation of a foreign jurisdiction that is effectively managed and controlled in the UAE | (3) three months from the end of the Financial Year of the person |

Tax Registration Deadlines of Non-Resident Juridical Persons

A juridical person, that is a Non-Resident Person prior to 1 March 2024, shall submit a Tax Registration application in accordance with the following:

Category of Juridical Persons | Deadline for submitting a Tax Registration application |

A person that has a Permanent Establishment in the UAE | (9) nine months from the date of existence of the Permanent Establishment |

A person that has a nexus in the UAE | (3) three months from the effective date of the FTA Decision |

A juridical person, that is a Non-Resident Person on or after 1 March 2024, shall submit a Tax Registration application in accordance with the following:

Category of Juridical Persons | Deadline for submitting a Tax Registration application |

A person that has a Permanent Establishment in the UAE | (6) six months from the date of existence of the Permanent Establishment |

A person that has a nexus in the UAE | (3) three months from the effective date of the FTA Decision |

Tax Registration Deadlines of Natural Persons

A natural person conducting a Business or Business Activity in the UAE shall submit a Tax Registration application in accordance with the following:

Category of Natural Persons | Deadline for submitting a Tax Registration application |

A Resident Person who is conducting a Business or Business Activity during the 2024 Gregorian calendar year or subsequent years whose total turnover derived in a Gregorian calendar year exceeds the threshold specified in the relevant tax legislation | 31 March of the subsequent Gregorian calendar year |

A Non-Resident Person who is conducting a Business or Business Activity during the 2024 Gregorian calendar year or subsequent years whose total turnover derived in a Gregorian calendar year exceeds the threshold specified in the relevant tax legislation | (3) months from the date of meeting the requirements of being subject to tax |

Penalties for Non-Compliance

On 27 February 2024, the Ministry of Finance issued Cabinet Decision No 10 of 2024 (amending the schedule of violations and administrative penalties of Cabinet Decision No 75 of 2023) that specifies that an administrative penalty of AED 10,000 will be imposed for failure to meet the deadlines provided for the submission of a tax registration application.

Points for Consideration

We suggest that you review and understand the registration timelines, and commence any necessary action to ensure compliance. Furthermore, Corporate Tax registration will now form part of any new corporate establishment process as, unlike VAT registration for which certain thresholds are required to be met, resident juridical entities will have only three months from the date of incorporation, establishment or recognition to submit an application for their Corporate Tax registration. ■

The Participation Exemption – Dividends and Capital Gains

Ownership of shares by companies usually results in tax being payable for dividends received or capital gains realised upon sale. However, in the UAE, the Corporate Tax law (Federal Decree No. 47 of 2022) (“CT Law”) provides an exemption to Corporate Tax in a certain scenario referred to as the Participation Exemption.

Article 23 of the CT Law states:

“Participation Exemption”

1. Income from a Participating Interest shall be exempt from Corporate Tax, subject to the conditions of this Article.

2. A Participating Interest means, a 5% (five percent) or greater ownership interest in the shares or capital of a juridical person, referred to as a “Participation” for the purposes of this Chapter where all of the following conditions are met:

a.) The Taxable Person has held, or has the intention to hold, the Participating Interest for an uninterrupted period of at least (12) twelve months.

b.) The Participation is subject to Corporate Tax or any other tax imposed under the applicable legislation of the country or territory in which the juridical person is resident which is of a similar character to Corporate Tax at a rate not less than the rate specified in paragraph (b) of Clause 1 of Article 3 of this Decree-Law.

c.) The ownership interest in the Participation entitles the Taxable Person to receive not less than 5% (five percent) of the profits available for distribution by the Participation, and not less than 5% (five percent) of the liquidation proceeds on cessation of the Participation.

d.) Not more than 50% (fifty percent) of the direct and indirect assets of the Participation consist of ownership interests or entitlements that would not have qualified for an exemption from Corporate Tax under this Article if held directly by the Taxable Person, subject to any conditions that may be prescribed under paragraph (e) of this Clause.

e.) Any other conditions as may be prescribed by the minister.

This Article provides that income from a Participating Interest, such as dividends and capital gains, is exempt from Corporate Tax. A Participating Interest is defined as a significant, long-term ownership interest in a juridical person (the Participation) that suggests some degree of control or influence over the Participation and that meets the conditions of this Article 23. With respect to dividends, Article 23 is usually used for dividends received by a UAE company (which is a Resident Person) from a foreign company. Dividends received from a UAE company (which is a Resident Person) are exempt from Corporate Tax with no further conditions (Article 22 (1) of the CT Law).

As an example, if a UAE Company owns a German Company (Participating Interest) and it receives dividends and later sells these shares and receives capital gains, then the dividend income and the capital gains income can be exempt from Corporate Tax if the following condition are met:

a.) the UAE company has held, or has the intention to hold, the Participating Interest for an uninterrupted period of at least (12) twelve months. The UAE Company should hold the shares of the German Company (Participating Interest) for an uninterrupted period of 12 months.

b.) The Participation must be subject to Corporate Tax (or equivalent) of 9% or more. This condition requires the Participation (ownership of shares by the UAE Company in UAE Company) to be subject to Corporate Tax or any other tax imposed under the applicable legislation of the country or territory in which the juridical person is resident which is of a similar character to Corporate Tax. In this case, it would be subject to Corporate Tax if it were not for this exemption and it would be subject to a similar or higher tax rate in Germany. Hence this test is satisfied.

c.) The ownership interest of the UAE Company in the Participation entitles the UAE Company to at least 5% of the profits and liquidation proceeds. In this case, the UAE Company would be entitled to 100% of the profits and liquidation proceeds of the German Company as the 100% owner. The ownership interest must entitle the UAE Company to at least 5% of the Participation’s profits available for distribution and at least 5% of the liquidation proceeds upon cessation of the Participation. As a result, this test is satisfied. Note that if the acquisition of the Participating Interest exceeds AED 4 million then this test is also satisfied (Ministerial Decision 116 of 2023).

d.) 50% or less of the assets of the Participation consist of non-qualifying ownership interests. An ownership interest in a Participation will be deemed a passive or portfolio investment that does not qualify for the Participation Exemption if 50% or more of the Participation’s assets, on a consolidated basis, consist of ownership interests or entitlements that by themselves do not meet the conditions of this Article had they been held directly by the Taxable Person.

Assets that would not qualify for the Participation Exemption include, for example, ownership interests in foreign juridical persons that are not subject to a corporate income tax in the relevant foreign jurisdiction, unless such ownership interests meet the conditions of Clause 3, or any other conditions as may be prescribed by the Minister under Clause 2(e).

In this case, the assets of the UAE Company that are shares in the German Company would be subject to tax in the UAE. Hence, the shares in the German Company are qualifying ownership interests which should satisfy this condition.

e.) The Participation Interest must meet any other conditions as may be prescribed by the Minister. As of the date of this memorandum, the other prescribed conditions are not relevant to these facts.

Based on the above, the following income (as specified under Article 23(5) of the CT Law) being capital gains and dividend income shall not be taken into account by the UAE Company in calculating its Taxable Income for Corporate Tax:

- Dividends and other profit distributions received from a foreign Participation that is not a Resident Person under paragraph (b) of Clause 3 of Article 11 of this Decree-Law.

- Gains or losses on the transfer, sale, or other disposition of a Participating Interest (or part thereof).

- Foreign exchange or impairment gains or losses in relation to a Participating Interest.

For the sake of illustrating the use of the Participation Exemption, the above analysis does not discuss the effects of any applicable double taxation treaty.

*****

Please contact Shahram Safai (ssafai@afridi-angell.com) if you require advice with respect to Corporate Taxation in the UAE. ■

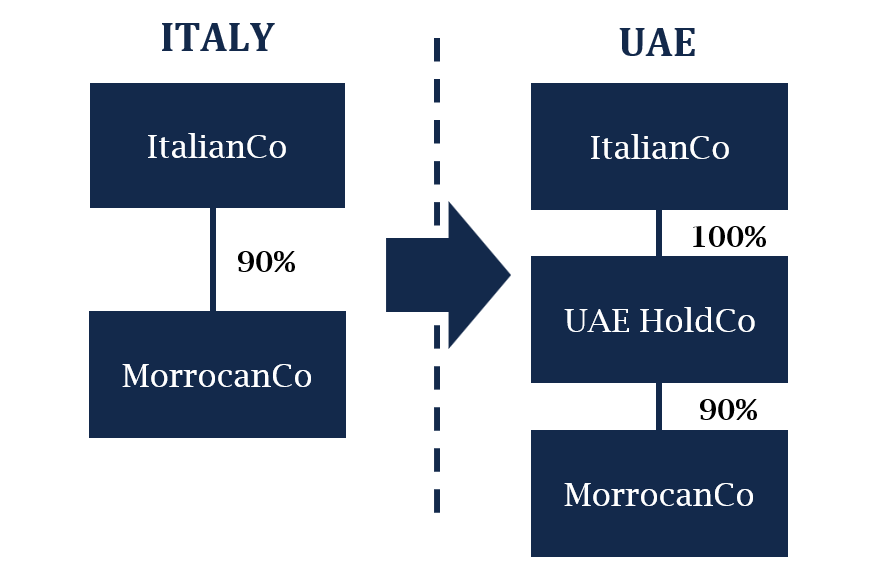

The Tax Benefits of using a UAE Free Zone Company as a Holding Company

UAE companies can offer significant tax benefits when used as holding companies in certain scenarios.

As an example, assume that an Italian limited liability company (“ItalianCo”) holds a 90% stake in a Moroccan operating subsidiary (“MoroccanCo”) and does not have a permanent establishment in Morocco. The ItalianCo is considering transferring its ownership in MoroccanCo to a wholly-owned holding entity located in the United Arab Emirates (“UAE HoldCo”).

Refer to the attached PDF for the full image of illustration

In this scenario, the ownership by a UAE free zone holding company (UAE HoldCo) of shares of a company that is established in another jurisdiction can be advantageous from a tax perspective, subject to the provisions of the applicable double taxation treaty. This is because in such holding of shares scenario, it is advantageous from a tax perspective (i.e. 0% tax rate on dividends, interest payments and capital gains received by the UAE HoldCo) for the UAE HoldCo to be a UAE free zone company, and specifically and according to the UAE Corporate Tax Law (Federal Decree Number 27 of 2022) (“CT Law”), for it to be a Qualifying Free Zone Person (with Qualifying Income).

The reasoning for the above is described below:

0% Tax Rate

Article 3 of the CT Law states:

“Corporate Tax shall be imposed on a Qualifying Free Zone Person at the following rates:

a.) 0% (zero percent) on Qualifying Income.

b.) 9% (nine percent) on Taxable Income that is not Qualifying Income under Article 18 of this Decree-Law and any decision issued by the Cabinet at the suggestion of the Minister in respect thereof.”

Hence the UAE HoldCo should be incorporated, firstly, as a Qualifying Free Zone Person (QFZP) that, secondly, should derive Qualifying Income to qualify for the 0% tax rate. We review both of these requirements in turn below.

Qualifying Free Zone Person

To be a Qualifying Free Zone Person, the provisions of Article 18 of the CT Law must be satisfied which state:

“Qualifying Free Zone Person

1. A Qualifying Free Zone Person is a Free Zone Person that meets all of the following conditions:

a) Maintains adequate substance in the State.

b) Derives Qualifying Income as specified in a decision issued by the Cabinet at the suggestion of the Minister.

c) Has not elected to be subject to Corporate Tax under Article 19 of this Decree-Law.

d) Complies with Articles 34 and 55 of this Decree-Law. [our note: Article 34 of the CT Law relates to Requirement of Arm’s Length Principle as between Related Parties) and Article 55 of the CT Law relates to Compliance with Transfer Pricing with Related Persons or Connected Persons of the CT Law].

e) Meets any other conditions as may be prescribed by the Minister.”

Accordingly, the definition of QFZP must also be satisfied by UAE Holdco as a Free Zone Person (a juridical person incorporated, established or otherwise registered in a UAE Free Zone). The most important practical component of the above definition is the deriving of Qualifying Income.

Qualifying Income

Qualifying Income is defined as follows in Cabinet Decision 55 of 2023 (“Cabinet Decision 55”):

“Article 3 – Qualifying Income.

1. For the purposes of application of Article (18) of the Corporate Tax Law, Qualifying Income of the Qualifying Free Zone Person shall include the below categories of income, provided that such income is not attributable to a Domestic Permanent Establishment or a Foreign Permanent Establishment in accordance with Article (5) of this Decision or to the ownership or exploitation of immovable property in accordance with Article (6) of this Decision:

(b) Income derived from transactions with a Non-Free Zone Person, but only in respect of Qualifying Activities that are not Excluded Activities …”

Accordingly, and pursuant to Article 3(1)(b) of Cabinet Decision 55, Qualifying Income of UAE HoldCo (as a QFZP) shall include income derived from transactions with a Non-Free Zone Person, but only in respect of Qualifying Activities that are not Excluded Activities (which should not be attributed to a Domestic Permanent Establishment, a Foreign Permanent Establishment or to the ownership or exploitation of immovable property).

As a result, income derived from UAE HoldCo’s ownership of MoroccanCo’s shares is Qualifying Income because it is income derived from transactions with MoroccanCo as a Non-Free Zone Person in respect of the Qualifying Activities of holding of shares of the MorrocanCo. Qualifying Activities are defined in Ministerial Decision No. 139 of 2023 (“Ministerial Decision 139”) as including the “holding of shares and other securities”.

Excluded Activities

As discussed, such Qualifying Activities should not be Excluded Activities, pursuant to Article 3(1)(b) of Cabinet Decision 55. Article 3 of Ministerial Decision 139 defines Excluded Activities to include activities related to (subject to certain exceptions) transactions with natural persons, banking activities that are subject to regulatory oversight, insurance activities that are subject to regulatory oversight, ownership or exploitation of immovable property and ownership or exploitation of intellectual property assets.

The holding of the MorrocanCo shares by UAE HoldCo is none of the foregoing which means that it is not Excluded Activities.

Hence in summary, and based on the above, UAE Holdco should derive Qualifying Income because it conducts Qualifying Activities (holding of shares of MoroccanCo) which are not Excluded Activities, and such income should not be attributable to a Domestic Permanent Establishment, a Foreign Permanent Establishment or immovable property.

***

Such UAE CT Law tax benefits provide significant opportunities for using UAE free zone companies as holding companies for foreign shares in order to reduce applicable taxes (i.e. possibly to 0% tax rate on dividends, interest payments and capital gains received by the UAE HoldCo with respect to ownership of such foreign shares) that may have otherwise been much higher in the foreign jurisdiction. ■

UAE Cabinet Decision No. (49) of 2023 dated 8 May 2023 (effective 1 June 2023)

UAE Cabinet Decision No. (49) of 2023 dated 8 May 2023 (effective 1 June 2023) states that for the purposes of Clause 6 of Article 11 of the Corporate Tax (CT) Law, Businesses or Business Activities conducted by a resident or non-resident natural person shall be subject to CT only where the total Turnover exceeds AED 1,000,000 for a calendar year. Importantly, the Decision also states that activities of resident or non-resident natural persons that result in Turnover from Wage, Personal Investment Income or Real Estate Investment Income shall not be considered Businesses or Business Activities that are subject to the CT Law. Therefore, such natural persons shall not be required to register for CT assuming they do not conduct any other Businesses or Business Activities that are subject to CT. ■

The Ministry of Finance publishes an Explanatory Guide on the Corporate Tax Law

Last Friday, on 12 May 2023, the UAE Ministry of Finance (Ministry) published an Explanatory Guide which provides an explanation of the meaning and intended effect of each article of the Corporate Tax (CT) Law. The Explanatory Guide may be accessed here.

The Introduction to the Explanatory Guide states that the Explanatory Guide may be used in interpreting the CT Law and how particular provisions of the CT Law may need to be applied, and that it must be read in conjunction with the CT Law and the relevant decisions issued by the Cabinet, the Ministry and the Federal Tax Authority. The Introduction also makes it clear that the Explanatory Guide is not meant to be a comprehensive description of the CT Law and its implementing decisions.

Some highlights of the Explanatory Guide include:

- For CT purposes, a civil company (which under the UAE Civil Code enjoys the status of a separate legal person) will not be treated as a separate legal person and be treated as the natural person or persons owning them because of their direct relationship and control over the Business and their unlimited liability for the debts and other obligations of the Business;

- Certain qualifying activities conducted by free zone persons are eligible for the zero percent CT benefit;

- Tax residency for CT purposes is not dependent on legal residency;

- No time limitation for carry forward of tax losses;

- Details transfer pricing documentation requirements and thresholds for maintaining master file and local file;

- Scope of ‘Qualifying Income’ for free zone establishments remain undefined; and

- Acknowledgement that taxpayers are permitted to optimize their tax position in a manner consistent with the CT Law.

The Afridi & Angell Tax Team is closely reviewing the 106-page Explanatory Guide and will continue to provide more details in the coming days. ■

Planning for Canada’s Departure Tax

We have written previously about the importance of planning for the tax consequences of emigrating from Canada; see our previous inBrief here. In this inBrief, we will describe a number of more advanced planning options for Canadian residents who are considering giving up their Canadian residency. Bear in mind that not all of the approaches discussed in this inBrief will be right for any particular person, as each person’s individual circumstances will differ.

Upon becoming a non-resident, Canada imposes a departure tax in the form of deemed disposition of certain capital assets, causing any unrealized capital gains to be realized in the year of departure. It is common for high net-worth individuals in Canada to hold their public and private investments through holding companies (Holdcos), so one major source of capital gains upon emigration is the shares they own in their Holdcos. We will also touch upon foreign trust planning, Canadian real estate holdings, and charitable donations.

With respect to Holdco shares, much emigration planning focuses on how to minimize the departure tax by reducing the fair market value of those shares prior to exit. Some potential options to achieve this may include.

Strategic Dividends: Causing Holdco to pay out dividends to the maximum extent it can out of tax-preferential accounts maintained by it, which may include Holdco’s capital dividend account (CDA), eligible refundable dividend tax on hand (ERDTOH) and non-eligible refundable dividend tax on hand (NERDTOH). Dividends can be paid out of Holdco’s CDA tax-free, and dividends that are paid out of its ERDTOH and NERDTOH result in tax refunds to the company, making them somewhat more tax-efficient. In advance of doing this, it may be advisable for Holdco to sell some of its investments, thereby realizing capital gains and creating additional CDA that can be dividend out tax free. The payment of dividends in this manner will reduce the fair market value of Holdco’s shares, thereby reducing the amount of the deemed capital gain on such shares upon emigration.

The other reason you should be sure to dividend out all CDA in any Holdco prior to emigration is because such dividends lose their tax-free status when paid to a non-resident shareholder. Once you are a non-resident, Holdco will be required to apply a withholding tax to any dividends paid to you, and you will be taxed on such dividends personally under the laws of your new country of residence. If Holdco will continue to operate after you emigrate and will continue to have Canadian resident shareholders, it would be prudent to create separate classes of shares that allow for dividends out of CDA to be paid to Canadian shareholders (who can receive them tax-free), and other dividends to be paid to you (as you may very well be in a position to receive them much more tax-efficiently than a Canadian shareholder[1]).

Life Insurance: Cause Holdco to acquire life insurance on your life, acquiring a policy that is maximum funded at the outset but with attributes that result in the policy having a low fair market value. This expenditure in exchange for an asset that is initially low-value (the life insurance policy) reduces the value of the Holdco shares. There are several other potential benefits to this approach that stem from the value of the insurance policy itself, because its value will increase after you have emigrated and can be leveraged as a valuable asset of Holdco going forward (i.e., front-end or back-end leveraging strategies to extract value from the policy during your life), in addition to the security of the death benefit.

If Holdco does leverage the life insurance policy by borrowing against it, Holdco will be able to use those funds for income-generating investments and will be permitted to deduct the interest on the loan. This can be an attractive arrangement.

You may wish to consider whether it makes sense to introduce a foreign ownership structure that is more forward-looking and supports your wealth and estate plans more broadly. For example, if you intend to establish a family trust structure in an offshore jurisdiction as part of your post-emigration planning, it may be prudent to transfer the shares of Holdco to the foreign trust at approximately the same time that you emigrate from Canada. You would do this after having taken any available steps to reduce the value of Holdco’s shares, as described above. If Holdco’s value is derived primarily from Canadian real estate holdings, this approach could be beneficial if you foresee a sale of Holdco in the future. In that case Holdco shares will be “taxable Canadian property” and will be taxed in Canada, and you can reduce the impact of that tax by reducing the value of Holdco’s shares through dividends after you are a non-resident (at the lower beneficial treaty rate).

There are special considerations with respect to Canadian real estate holdings. Canadian real estate is “taxable Canadian property” and is not subject to the deemed disposition upon emigration.[2] How you can best structure your holding of Canadian real estate as a non-resident will depend on whether it is property for your personal use, or if it is a rental property. If it is for personal use, you will need to consider whether your ownership of it puts you at risk of being deemed to be Canadian resident for tax purposes even after your emigration.[3] If it is a rental property, you will likely wish to transfer ownership of it to a Canadian holding company, otherwise the tenant will be required to withhold an amount in respect of tax from every rent payment they make to you as a non-resident owner.

Finally, an option that is not to be overlooked is simply making a charitable donation of assets that have significant accrued capital gains before you emigrate, which will have the effect of reducing both the value of your holdings as well as reducing your departure tax exposure. It will also generate a charitable tax credit which you may use to further reduce your tax burden on exit. If your charitable intentions are relatively large and you wish to maintain some ongoing involvement and control over the how the endowment is managed, you may wish to establish a charitable foundation instead of simply donating funds or assets to an existing charity. A charitable foundation that is registered as such with the Canada Revenue Agency will qualify as a registered charity and can issue charitable tax receipts, and can carry out activities and funding in line with its charitable purpose in Canada and overseas. The charitable options should, of course, only be considered where the primary objective is furthering the chosen charitable purpose with any tax incentives being secondary.

The strategies discussed in this inBrief are intended to illustrate that there may be effective pre-emigration planning that you can consider, aimed at reducing the impact of Canada’s departure tax. All such strategies are complex in their planning and application and professional advice is required to evaluate and execute them. If you are interested in exploring planning of this nature, please contact us and we will be delighted to assist. ■

—

[1] The withholding tax that Holdco would be required to apply to dividends paid to you as a non-resident would be a default rate of 25% if you reside in a non-treaty country, or could be 5%, 10% or 15% if you reside in a treaty country. You may need to hold your shares through a company established in your new country of residency to access these reduced rates.

[2] You may elect to trigger a deemed disposition of taxable Canadian property if you prefer, in order to trigger gains or losses which you are able to offset against other losses or gains on exit, respectively.

[3] Very briefly, owning a residential property which is available for your personal use in Canada will cause you to be deemed tax resident in Canada, unless there are tie-breaker rules in the applicable treaty with your new country of residence. Ensuring that you will indeed be non-resident for tax purposes is a critical aspect of non-residency planning.